Pensions: Ugh, Again?!

Dear Corporate Pension Plan Sponsors,

Pensions are again climbing up the list of priorities for corporate treasurers, as the funded status of defined-benefit pension plans is once again within spitting distance of all-time lows. Funded status dropped during Q2 2016 by about 2% to the mid-70s on a percentage basis for the average S&P 500 plan.

Treasurers should ask themselves 3 questions: (1) are PBGC variable-rate premiums starting to bite, (2) would a debt-funded pension contribution before year-end make economic sense, and (3) does the drop to record lows for long-term U.S. Treasury yields call for a reassessment of pension strategy?

1. Are PBGC variable-rate premiums starting to bite?

PBGC premiums are effectively a tax on the plan sponsor that does not benefit the plan itself, which is why many companies seek to minimize the cost. The recent drop in interest rates and resulting rise in pension liabilities will snag many companies into owing variable-rate premiums for the first time.

What can a corporate treasurer do?

Because variable-rate premiums are tied to “unfunded vested benefits,” companies can reduce this cost by funding some or all of the plan’s unfunded vested benefits. Several innovative funding structures can help plan sponsors minimize variable-rate premiums without permanently trapping cash.

Many companies will now start solving to minimize the amount of variable-rate premiums owed when determining their pension contribution strategy. This is a big change, since for years the real constraint on pension funding decisions for most companies had been the leverage concerns of rating agencies and investors. Statutory funding requirements have been watered down by interest rate smoothing mechanisms enacted by Congress post-crisis, so much so that minimum required contributions had not been the binding constraint for most companies in recent years.

The “corridor” that smoothes interest rates for funding calculation purposes does not apply to variable-rate premium calculations, which is why so many companies will now owe variable-rate premiums amid record low long-term interest rates.

And their cost can be substantial. Variable-rate premiums jumped this year to $30 from $24 per $1,000 of unfunded vested benefits, plus another $1 due to inflation indexation.

2. Debt-funded discretionary contributions: return of a market trend?

Unless interest rates rise substantially during the third quarter, I would expect debt-funded pension contributions to return en masse during the fourth quarter as companies shore up pension plans before the year-end valuation date.

The environment for issuing long-term debt to fund pension contributions is ideal for many companies: record low long-term Treasury yields and tight corporate spreads. Cost savings from avoiding PBGC variable-rate premiums help make the net-present value calculation positive—but the math is always company-specific.

3. Should you reassess pension strategy given record low long-term Treasury yields?

In my inaugural pension blog post from April, I encouraged corporate treasurers to think through what would happen to your company’s capital structure if interest rates go negative and your pension liability balloons. The urgency of this exercise has increased in light of recent events.

As a reminder, U.S. corporate pension obligations rank “super-senior” within corporate capital structures (i.e., they come first in line, pretty much). When interest rates drop and the pension liability grows, the pension’s implicit claim on corporate assets grows—and if the pension liability grows faster than corporate assets grow, it means fewer corporate assets would be available to the debtholders and stockholders (who rank below the pension). This explains why stock prices and bond spreads of companies with big pension liabilities tend to lag or correct when interest rates drop.

I’ll close with the following discussion about interest rates, meant to be thought-provoking.

Again, no investment advice on this blog!

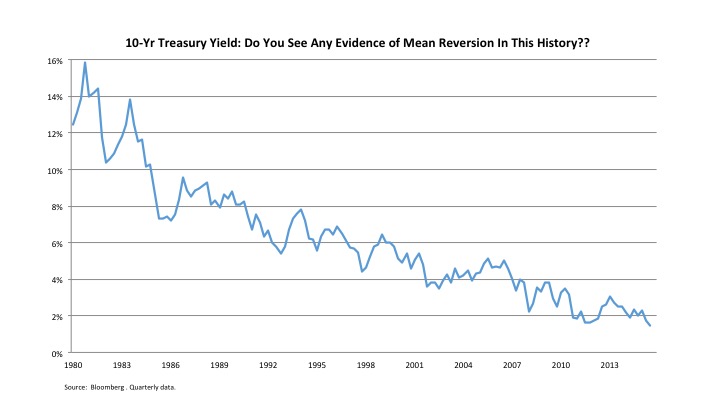

Here’s a quarterly chart of the U.S. 10-year Treasury yield. Not once since 1980 has the 10-year Treasury yield risen above its prior peak during a rising interest rate cycle, before rates turned lower again as wheels came off somewhere in the economy. Now it’s happening again, as futures markets are implying the Fed’s rate rising cycle may already be over and markets are starting to imply a non-zero probability of rate cuts.

What do you see in the 10-year Treasury yield chart? I see an unbroken trend of lower lows and lower highs across 36 years of interest rate cycles. Yet, the consensus believes interest rates are mean-reverting and will move higher over time. Do you see evidence of that?

In the spirit of a “four corners of the problem” analysis, calculate what would happen if the discount rate on your pension plans went to zero and stayed there for infinity. How many of your corporate assets would implicitly belong to pensioners, and how many (if any) would be left for stakeholders who rank junior to pensioners in the capital structure?

The entire Swiss yield curve, out to 50 years, now has negative yields. If this doesn’t normalize, does this mean—in the coming years—we will see impairments in the carrying value of multinational companies’ Swiss subsidiaries that have material pension obligations?

The good news? There’s plenty of time for corporate treasurers to plan ahead! I’m expressly making no forecasts in this blog post—only encouraging companies to reach a “no regrets later” consensus about pension strategy in light of record low interest rates. If you knew that the Swiss situation would hit the U.S. in X number of years, what would you wish you’d done differently today? How much interest rate risk should your company’s capital structure take? Would you fund the pension plan differently, manage interest rate risk differently, or more aggressively pursue lump sums or risk transfer strategies?

It’s all worth pondering and scenario-planning.

Let’s hope you never need that plan!

This blog post is for plan sponsor use only. It is not intended as investment advice. The author is not providing services to any employee benefit plan, including as fiduciary or advisor to any employee benefit plan, and should not be mischaracterized as such. Please see important additional disclosures here. Thank you for stopping by my website!

Founder/CEO Custodia Bank. #bitcoin since 2012. 22-yr Wall St veteran. Not advice; not views of Custodia Bank!

Disclaimer

This web site is limited to the dissemination of general information, investment-related information, publications, and links.

Please consult important additional information and qualifications HERE.

View Privacy Policy and Terms of Use